Financial Plan from Scratch for 2025

Taking a look at my general strategy to financial planning.

Getting Started: The Financial Plan

I remember reading Rich Dad Poor Dad many years ago and a quote that has always stuck out for me was “The rich pay themselves first and pay others second”. So personally I like starting with mapping out what my income for the year is then apply my target savings percentage.

Looking at an example, if I make $120,000 a year living in Ontario and my target savings rate is 20% I need to save $24,000.

Let’s pretend I am early in my financial freedom odyssey and have plenty of RRSP and TFSA space. Let’s also say I have an emergency fund built up already.

I choose to use the dollar cost averaging approach and contribute $1,000 to my TFSA and $1,000 to my RRSP each month. (Perhaps the TFSA midway through and the RRSP at the end of the month 😉)

Now that I have my financial plan in place (save and invest 20% of my gross income). I need to create a budget to ensure that I will be able to stick to the plan.

The Budget

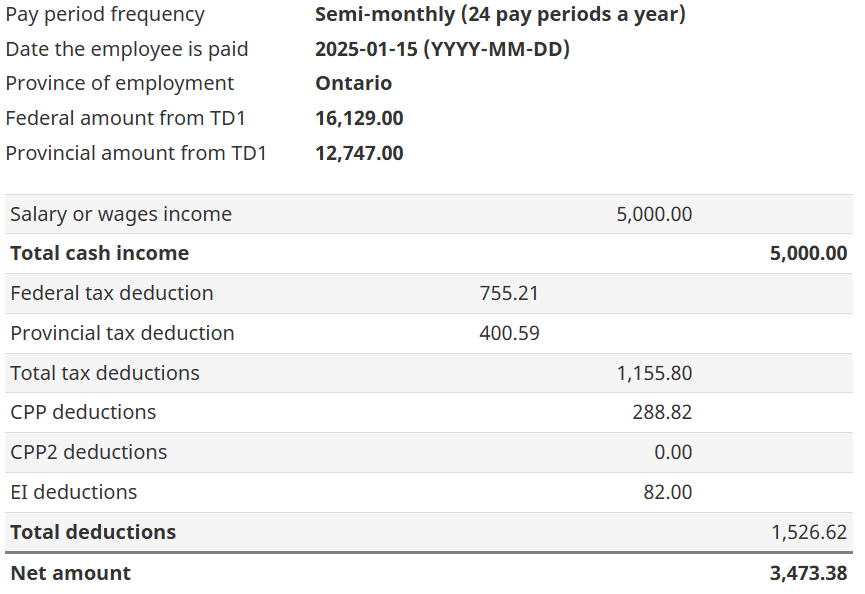

Next I need to know what my take home would be and for that I can jump over to the CRAs calculator called PDOC. Assuming you get paid twice a month and have 0 deductions outside of tax $120,000 / 24 pay cheques = $5,000 per pay before taxes

Entering that information we see a take home pay of $3,473.38 per pay cheque or $6,946.76 a month:

Not to dive too deep into how taxes work but at this income you will reach both the EI and CPP maximum contributions part way through the year and thus will receive a higher net pay at the end of the year. I will always recommend increasing your contributions to your registered accounts, but, the choice is yours!

| Line Item Name | Line Item Amount |

|---|---|

| Pay Cheques | $6,946.76 |

| TFSA Contribution | $1,000.00 |

| RRSP Contribution | $1,000.00 |

| Remainder: | $4,946.76 |

Adding the essentials into your budget

Now that we have paid ourselves first let’s add our essentials like food, rent and utilities. I’m not sure if utilities include internet yet but in my mind it 100% does.

| Line Item Name | Line Item Amount |

|---|---|

| Remainder from Previous Section | $4,946.76 |

| Rent (GTA AVG TREBB 1 Bedroom Condo) | -$2,499.00 |

| Groceries | -$600.00 |

| Personal Care | -$100.00 |

| Phone | -$100.00 |

| Internet | -$75.00 |

| Student Loans | -$300.00 |

| Electric | -$80.00 |

| Gas | -$75.00 |

| Transit Pass | -$143.00 |

| Rental Insurance | -$25.00 |

| Remainder: | $949.76 |

Add in some nice to haves and see what we have left for entertainment

| Line Item Name | Line Item Amount |

|---|---|

| Remainder from Previous Section | $949.76 |

| Life Insurance | -$50.00 |

| Subscription Services | -$75.00 |

| Rainy Day Fund 5% of take home | -$350.00 |

| Discretionary Remainder | $474.76 |

Personally I would like to set the rainy day fund to be slightly higher maybe target $500 per month, but, the choice is yours. Another tip is that you don’t have to spend the entirety of what is left over 😉

Budgeting and creating a financial plan can be this simple the important thing is to start, pay yourself first and then add items in terms of essentials, nice to haves and the rest is gravy.

Summary

Combining the previous sections we are left for with the following plan / budget.

| Line Item Name | Line Item Amount |

|---|---|

| Pay Cheques | $6,946.76 |

| TFSA Contribution | -$1,000.00 |

| RRSP Contribution | -$1,000.00 |

| Rent (GTA AVG TREBB 1 Bedroom Condo) | -$2,499.00 |

| Groceries | -$600.00 |

| Personal Care | -$100.00 |

| Phone | -$100.00 |

| Internet | -$75.00 |

| Student Loans | -$300.00 |

| Electric | -$80.00 |

| Gas | -$75.00 |

| Transit Pass | -$143.00 |

| Rental Insurance | -$25.00 |

| Life Insurance | -$50.00 |

| Subscription Services | -$75.00 |

| Rainy Day Fund 5% of take home | -$350.00 |

| Discretionary Remainder | $474.76 |

- the table above can easily be copied and pasted into google sheets to get you started!

While this may seem overly simple it is extremely close to how I budgeted in the early years of my career. Although I was making significantly less, sharing a 2 bedroom apartment and contributing far less than $1000 to my TFSA and RRSP.

I would suggest making a spreadsheet and tracking all of your expenses for the entirety of 2025 to get a true picture and who knows maybe a few areas for improvement will reveal themselves.

Now that I am married, we are paying off a mortgage, have a car etc, my approach to budgeting and financial planning has taken a slightly more complex form which I will reveal next week! Enjoy your week and I hope I see you here on Monday.

You can support me by:

- Subscribing to my YouTube Channel

- Using my WealthSimple referral link

- Simply continuing to read my weekly posts here!

Cheers ☕